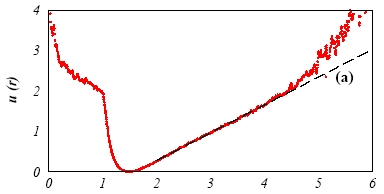

We characterize the collective phenomena of a liquid market. By interpreting the behavior of a no-arbitrage N asset market in terms of a particle system scenario, (thermo)dynamical-like properties can be extracted from the asset kinetics. In this scheme the mechanisms of the particle interaction can be widely investigated. We test the verisimilitude of our construction on two-decade stock market daily data (DAX30) and show the result obtained for the interaction potential among asset pairs.

We characterize the collective phenomena of a liquid market. By interpreting the behavior of a no-arbitrage N asset market in terms of a particle system scenario, (thermo)dynamical-like properties can be extracted from the asset kinetics. In this scheme the mechanisms of the particle interaction can be widely investigated. We test the verisimilitude of our construction on two-decade stock market daily data (DAX30) and show the result obtained for the interaction potential among asset pairs.