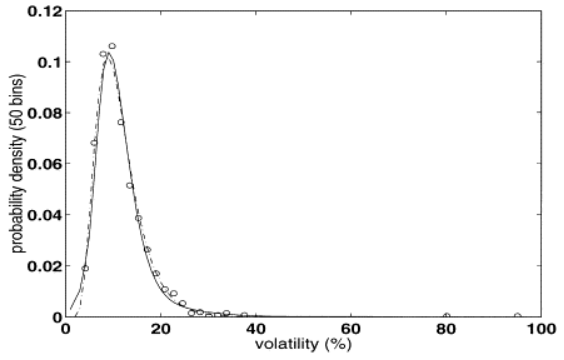

We study the volatility of the MIB30-stock-index high-frequency data from November 28, 1994 through September 15, 1995. Our aim is to empirically characterize the volatility random walk in the framework of continuous-time finance. To this end, we compute the index volatility by means of the log-return standard deviation. We choose an hourly time window in order to investigate intraday properties of volatility. A periodic component is found for the hourly time window, in agreement with previous observations. Fluctuations are studied by means of detrended fluctuation analysis, and we detect long-range correlations. Volatility values are log-stable distributed. We discuss the implications of these results for stochastic volatility modelling.

We study the volatility of the MIB30-stock-index high-frequency data from November 28, 1994 through September 15, 1995. Our aim is to empirically characterize the volatility random walk in the framework of continuous-time finance. To this end, we compute the index volatility by means of the log-return standard deviation. We choose an hourly time window in order to investigate intraday properties of volatility. A periodic component is found for the hourly time window, in agreement with previous observations. Fluctuations are studied by means of detrended fluctuation analysis, and we detect long-range correlations. Volatility values are log-stable distributed. We discuss the implications of these results for stochastic volatility modelling.